- 06/03/2026

- by Mathu Govintan

- GST

- 803 Views

- 0 Comments

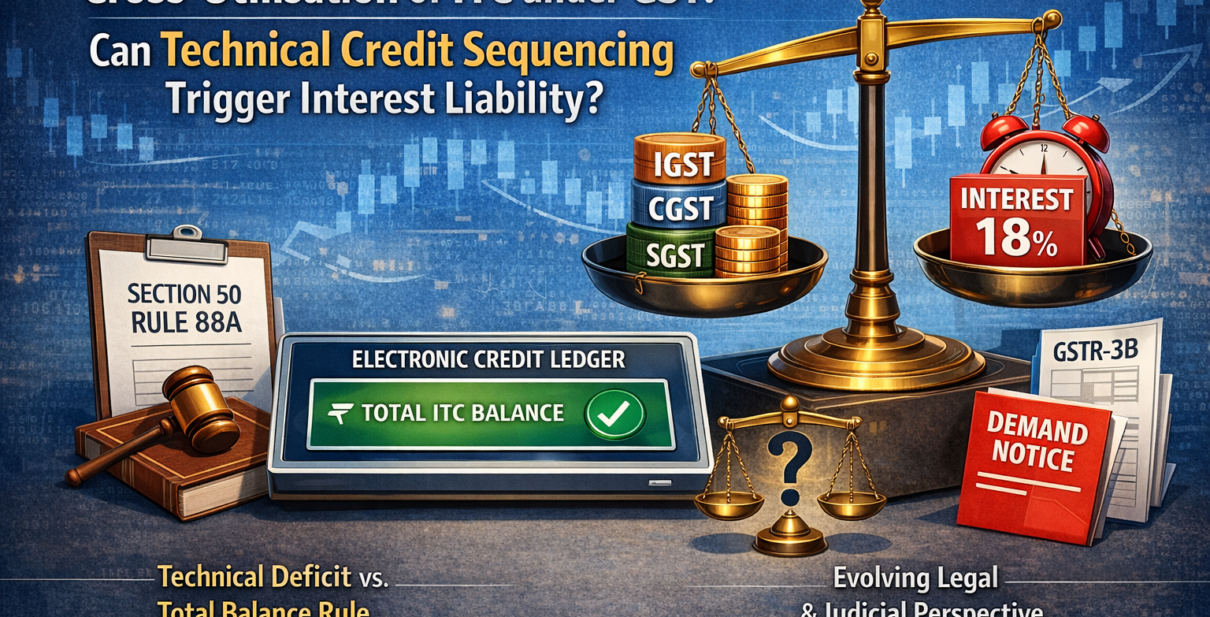

Cross-Utilisation of ITC under GST: Can Technical Credit Sequencing Trigger Interest Liability?

The Goods and Services Tax (GST) architecture is built upon the seamless flow of Input Tax Credit (ITC). However, the introduction of Section 49A and Rule 88A mandated a strict technical sequencing of credit utilization i.e., Integrated GST (IGST) credit must be entirely exhausted before Central GST (CGST) or State GST (SGST) credits can be touched. This rigid hierarchy often creates a probable “technical” deficit in one tax head even when the taxpayer has a massive surplus in another. The pivotal legal question is

Whether a shortfall in a specific ledger caused solely by this mandatory sequencing can trigger interest liability under Section 50, even if the taxpayer’s total electronic credit pool remains positive ?

The Legal Position refers to Section 50 and Rule 88A of CGST Laws.

Under the legal framework of Section 50(3) of the CGST Act (read along with all retrospective amendments), interest is only leviable when ITC has been “wrongly availed and utilized.”

For years, the Department maintained a “head-wise” approach, arguing that if you had a shortfall in the IGST ledger, you owed interest on that specific deficit. However, the law evolved through Circular No. 192/04/2023, which clarified the “Total Balance” rule.

It established that for the purpose of calculating interest, the aggregate balance of ITC in the Electronic Credit Ledger (IGST + CGST + SGST) must be considered. If the total balance remains higher than the “wrongly availed” amount, no interest is triggered, effectively shielding taxpayers from the pitfalls of technical sequencing.

The judiciary also has frequently intervened to ensure that interest which is compensatory in nature is not used as a penalty for procedural sequencing. In the landmark case of M/s. Eicher Motors Ltd vs. Superintendent of GST, the Madras High Court ruled that the “as and when” credit is available in the ledger, it is deemed to be in the possession of the State. Therefore, the technical act of debiting the ledger (which follows the sequencing rules) is merely a matter of accounting. Similarly, in the case of Refex Industries, the courts emphasized that interest is only payable on the “cash component” of the tax paid late. These precedents collectively argue that if the Exchequer is not deprived of funds, the technical order of using those funds cannot be a ground for interest.

Practically let us see a few instances which Trigger Interest Liabilities.

Despite the protective rulings, there are specific instances where interest liability still remains a potent threat.

First, interest is triggered if the total aggregate balance in the Electronic Credit Ledger falls below the amount of wrongly availed ITC; in this case, the sequencing becomes irrelevant because there is a genuine deficit in the “pool.”

Second, interest applies if a taxpayer is forced to pay tax through the Electronic Cash Ledger due to a delay in filing GSTR-3B, as interest is calculated on the net cash liability.

Third, if a taxpayer wrongly utilizes credit from one head to pay a liability that was ineligible for ITC (such as blocked credits under Section 17(5), etc.,), the sequencing cannot save them from an 18% interest charge.

Well……..

While technical credit sequencing dictates the “how” of tax payment, it should not dictate the “how much” of interest liability.

The current legal consensus is that interest is a restitutionary measure meant to compensate the Government for the actual loss of revenue. Since the GST portal’s sequencing rules are a procedural requirement rather than a substantive tax obligation, a mere mismatch in head-wise balances provided the total ITC pool is sufficient and should not trigger interest.

Taxpayers must, however, remain vigilant in maintaining a robust audit trail of their total credit balances to defend against any probable automated notices triggered by the portal’s such sequencing logic.